When credit card payment protection fails the purchaser due to a payment processing loophole

The following information on how credit-card payment protection can fail due to a loophole is unknown to many purchasers, including myself until I came across a feature on the BBC programme Rip Off Britain. Ignorance that loophole could cost purchasers of goods and services a fortune if they are under the *mistaken impression* that using a credit card for purchases over £100 and under £30,000 always provides payment protection from the credit-card company.

In this article, I deal with the loophole that exists in the UK, but it’s the kind of loophole that would benefit credit-card companies operating all over the world and, as such, probably exists in law where the rule of law operates. Therefore, wherever you live, you should ask the supplier if you have credit-card-payment protection *before* you make expensive purchases of goods and services.

Payment protection fails when using a third-party payment processing company

The advice to purchasers is to buy goods with a credit card, not a debit card. Because only a credit card provides payment protection if the goods never arrive, or the seller goes out of business, or the goods are faulty and the seller won’t replace the goods or make a refund, etc. Fortunately, that advice is not strictly true.

“Debit card purchases are not covered by Section 75 because they are not part of a credit agreement. But they do protect your purchases through the Chargeback scheme.”

Is debit card protection the same as for credit cards? –

https://www.money.co.uk/current-accounts/is-debit-card-protection-the-same-as-for-credit-cards.htm

That said, credit-card companies are increasingly refusing to refund the purchaser if something of that sort goes wrong if the payment is made to the retailer via a third-party payment-processing company, such as PayPal, Worldpay, Sage Pay, Creditcall, Stripe, etc.

Section 75 of the Consumer Credit Act

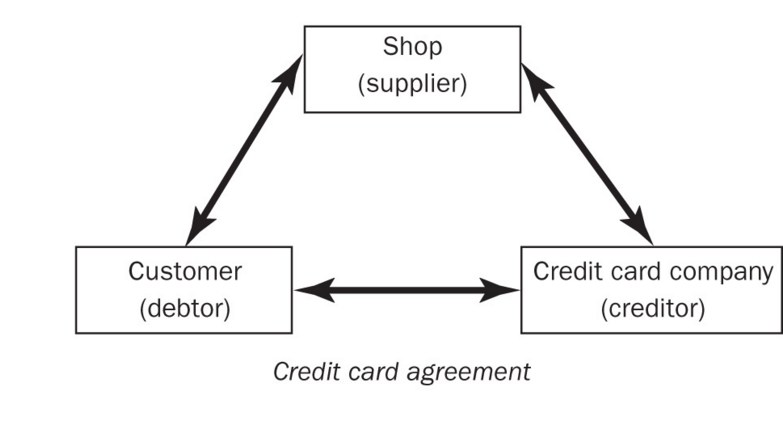

Section 75 of the Consumer Credit Act in the UK provides the consumer with credit-card purchase protection for goods costing more then £100 and less than £30,000. Both the vendor/supplier/manufacturer that sold the goods and the credit card company are jointly and severally (separately) liable if things go wrong. You would claim a repayment from the seller, but if it goes bust, you can claim a refund from the credit-card company.

Section 75 protection is available for purchases made abroad using you credit card. If you can’t get a refund from the seller, you should be able to do so from your credit card company. The protection is available for up to six years after making the credit-card purchase and is valid even if you no longer use that credit-card account.

Therefore, unless your credit-card company states in its terms and conditions that it will honour its Section 75 commitments if third-party payment companies accept the payments, Section 75 only gives protection if a direct relationship exits between you (the debtor), and the supplier (the creditor).

The Financial Ombudsman Service wants to close this loophole

In October 2016, the UK’s Financial Ombudsman Service (FOS) asked the Law Commission to reform Section 75 to embody third-party payments. Apparently, the Law Commission is going to present a short list of legal reforms that includes how third-party payments affect Section 75 some time in 2017. However, this may never happen. If it does, I will update this article.

Needless to say, if you are going to make expensive purchases using a credit card, you should find out how the payment via your credit card takes place and if it only uses a third-part company or companies, what your rights are under section 75.

It is the Financial Ombudsman Service that passes judgement in Section 75 disputes. This is UK law, so, as you might expect, even it is unable to provide clear guidance. Apparently, payment protection might or might not apply when a retailer uses third-party payment companies. Moreover, it won’t say which type of payment does or does not provide protection.

The following article provides some extra information on this serious loophole in the UK consumer protection.

Revealed: Section 75 credit card protection may fail due to payment processing loophole – shoppers beware –

https://www.moneysavingexpert.com/news/cards/2017/04/…

Here is the latest information on Section 75:

Section 75 Refunds – Free protection for credit card spending on items over £100 [December 2020] –

https://www.moneysavingexpert.com/reclaim/section75-protect-your-purchases/

Warning! Don’t use PayPal to pay on a credit card – You’re losing valuable Section 75 rights –

https://www.moneysavingexpert.com/credit-cards/PayPal-Section75/